Understanding FICO Scores: How to Improve Your Creditworthiness

Understanding FICO Scores: How to Improve Your Creditworthiness

A FICO score is a credit score that was developed by the Fair Isaac Corporation (FICO) and is widely used by lenders to determine creditworthiness. This score ranges from 300 to 850, with higher scores indicating better creditworthiness.

How is a FICO Score Calculated?

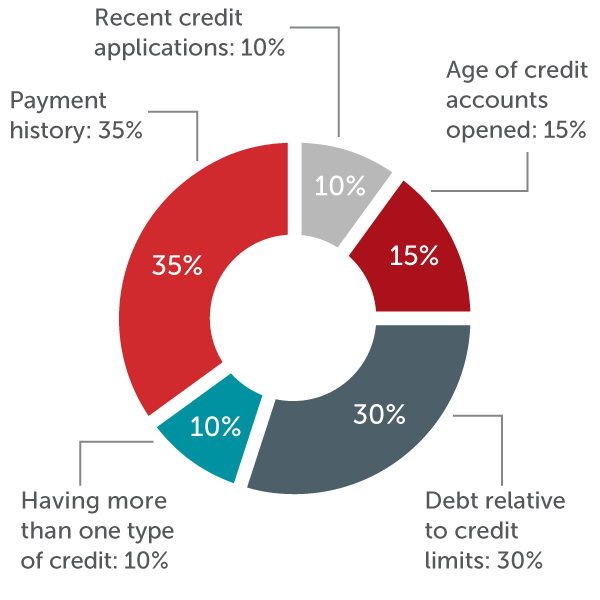

A FICO score is calculated using several factors that include payment history, amounts owed, length of credit history, credit mix, and new credit. Payment history carries the most weight, making up 35% of the score, while amounts owed makes up 30%, length of credit history makes up 15%, credit mix makes up 10%, and new credit makes up the remaining 10%.

Payment History

Payment history is the most important factor in determining a FICO score. Late payments, delinquent accounts, and bankruptcies can all negatively impact this score. A history of on-time payments, however, can improve it.

Amounts Owed

The amounts owed factor takes into account how much credit a person is using compared to their available credit. It also considers the total amount owed and the number of accounts with balances. High credit card balances can negatively impact this factor.

Length of Credit History

The length of credit history considers how long a person has had credit accounts and when they were last used. The longer a person has had credit and the more recently they used it, the better this factor is for their FICO score.

Credit Mix

Credit mix takes into account the types of credit a person has, such as credit cards, mortgages, and car loans. Having a mix of credit types can improve this factor.

New Credit

New credit considers the number of new accounts a person has opened and the number of recent credit inquiries. Opening too many new accounts or having too many inquiries can negatively impact this factor.

Why is a FICO Score Important?

A FICO score is important because it can impact a person's ability to obtain credit, such as loans or credit cards. It can also impact the interest rates they receive on those loans and credit cards. A higher score can result in better interest rates, while a lower score can result in higher interest rates or even denial of credit.

How Can a Person Improve Their FICO Score?

Improving a FICO score takes time and effort. The best way to improve a FICO score is to pay bills on time, keep credit card balances low, and avoid opening new credit accounts. It is also important to regularly check credit reports for errors and dispute any inaccuracies.

Conclusion

In summary, a FICO score is a credit score that lenders use to determine creditworthiness. It is calculated using several factors, including payment history, amounts owed, length of credit history, credit mix, and new credit. A higher score can result in better interest rates and access to credit, while a lower score can result in higher interest rates or even denial of credit. Improving a FICO score takes time and effort, but paying bills on time, keeping credit card balances low, and avoiding new credit accounts can all help.